The information provided here should serve as a foundation; school business officials should check with their auditors or payroll software vendors for detailed guidance on payroll and payroll systems.

Income

Employees’ income is divided into pensionable and non-pensionable (extra) income. What constitutes pensionable income versus extra pay depends on the individual state pension system. If you are unsure, check with your auditor. Additional pay has set federal withholding rates (www.irs.gov/pub/irs-pdf/p15.pdf).

Overtime/daily rate. Federal overtime provisions are included in the Fair Labor Standards Act (FLSA). Unless exempt, employees covered by the Act must receive overtime pay for working more than 40 hours in a workweek, at a rate not less than time and one-half their regular rates of pay. The FLSA does not require overtime pay for work on Saturdays, Sundays, holidays, or regular days of rest, unless overtime is worked on such days.

Different workweeks may be established for different employees or groups of employees. Typically, overtime pay earned in a particular workweek must be paid on the regular payday for the pay period in which the wages were earned.

On May 20, 2020, the U.S. Department of Labor announced a final rule that allows employers to pay bonuses or other incentive-based pay to salaried, nonexempt employees whose hours vary from week to week. The Department of Labor provides detailed information regarding this area (www.dol.gov/agencies/whd/overtime).

Sick/vacation pay upon retirement/termination of employment. The FLSA does not require organizations to pay employees for time not worked, such as vacations, sick leave, or holidays. These benefits are matters of agreement between an employer and an employee (or the employee’s representative).

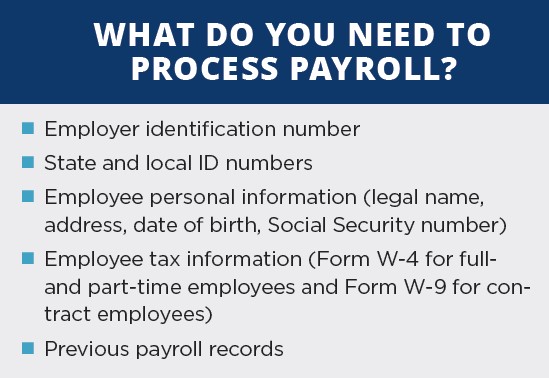

Payroll is one of the many areas that fall under the umbrella of the school business office.

The FLSA does not require severance pay either. It, too, is a matter of agreement between an employer and an employee (or the employee’s representative). Payout options may include a check or payment to a tax-sheltered annuity. Such payments are made after the employee has “left the building.”

ANDREY POPOV/STOCK.ADOBE.COM

ANDREY POPOV/STOCK.ADOBE.COM

Withholdings and Deductions

The two main types of payroll deductions are taxes and payroll withholdings. All school employees are subject to federal and state taxes with amounts withheld on the basis of W-4 paperwork. State disability may or may not be deducted depending on the statute. FICA

(Federal Insurance Contributions Act) and Medicare have employer share responsibilities. Other types of deductions include insurance policy deductions and retirement deductions. Payroll withholdings may include union dues.

Pension. Most school employees should be enrolled in a state pension system. Individual state pension websites are comprehensive with answers and guidance for employers.

Tax-sheltered annuities. Most districts allow participation in tax-sheltered annuities— 403(b) and 457 pretax (federal only) deduction savings plans. Each plan has federal limits. Since they are regulated, use a third-party administrator (TPA) for these programs.

In the past, the district administrator was the point person for signing off on transfers, loans, and withdrawals, among others. The compliance regulations are getting tighter, so if the district does not have a TPA, now might be a good time to explore using one.

Dues. When an employee is eligible to join the union, the building representative handles the completion and remittance of the paperwork, a copy of which is sent to payroll. Dues withholding begins upon approval from the state union. Any changes to dues are reflected in a form the district sends to the state union association.

Credit union deduction. Employees who participate in a credit union can have a portion of their income deposited into their credit union account.

Garnishments. Occasionally, the payroll office may receive information regarding a wage garnishment for such items as alimony, child support, or student loan default. Usually, the garnishment is a set amount or percentage per pay period. The payroll office must maintain the payment schedule until it receives notification that the garnishment has been satisfied.

Employee benefits. These deductions account for all benefits contributions from each employee. They include employer-sponsored retirement plans, health insurance, life insurance, and flexible spending accounts. There is a monthly fee for the flexible spending account that is usually passed through to the employee.

Other Considerations

In addition, direct deposit and other reporting items need attention.

Direct deposit. Most payroll systems can split net payroll checks into multiple checking and savings accounts. With the increase in cyber fraud, all direct deposit changes (especially changing banks) should be done in person, not through email.

Other reporting. On the 15th of each month, the payroll office files a report to the U.S. Department of Labor. On the 30th of each month the district is required to report to the state site all new employees (for child support purposes).

Attention to Detail

The auditors will spend time on payroll and agency. Make sure that contracts align to payroll and that you have documentation for everything (including errors). Payroll is 80% of your budget; when something goes wrong, it becomes a total headache (and your problem). Having a working knowledge of the moving parts that constitute each payroll run can lessen your stress if any issues arise. If you have any questions or concerns, reach out to your fellow business administrators.